Hey, where’s those so-called “waste-cutting” DOGE minions when you actually need them?

Santa Trump and his oligarch-led administration just gave their corporate donors who run Medicare (Taking) Advantage plans an early Christmas present – a $46 BILLION dollar rate hike.

Wanna save money? Stop rewarding Health insurers like Cigna, Aetna, and UnitedHealthcare and their mult-millionaire CEOs. (check out their compensation here!). Their business model relies on denying care to enrollees; (almost 23% of post-acute care requests) and their wasteful, insurance bureaucracy consumes about 14 percent of revenues, sevenfold higher than traditional Medicare’s 2 percent overhead. These are also the same miscreants who’ve been overcharging us taxpayers over $140 BILLION dollars annually through their plans, and they routinely drop benefits and policies for the seriously ill, minority groups, and for those in rural areas.

Action: Tell your legislators that we are tired of giving our taxes to these private insurance companies.

Example script for phone calls: I’m calling from [zip code] and I’m very upset to see that the donors behind Medicare Advantage plans, who have ripped off American taxpayers for billions, are getting a rate hike, while Congress is planning on stripping down Medicaid benefits, endangering health care for millions of us.

It’s time to sunset Medicare Advantage programs as a bad deal, and put their 14% profits into benefits for regular Medicare, so all America’s seniors can access vision, dental and hearing services.

Then, let’s join nations like Canada and Greenland and provide a publicly financed, non-profit single-payer national health program that would fully cover medical care for all Americans. I want to see [legislator’s name] on the cosponsor list for Rep. Jayapal’s upcoming Medicare-for-All bill.

Examples of emails from PNHP:

Subject: Don’t cut Medicaid. Cut subsidies to corporate health insurance instead.

I am writing to you as a constituent who is concerned about the future of Medicare and Medicaid.

I am especially concerned by reports that Congress is considering significant cuts to Medicaid in order to pay for an additional round of tax cuts. This crucial public health program has been a lifeline for low-income Americans for decades, and states that have chosen to expand the program in recent years have seen gains in both population health relative to non-expansion states and financial stability for their safety net hospitals and clinics.

When the Affordable Care Act was signed into law in 2010, the federal government promised to fully fund Medicaid expansion for the first three years and to fund 90% of Medicaid expansion from 2020 onwards. This is a promise that must be kept. To do otherwise—to reduce federal funding to 70%, 50%, or even lower—would starve an already cash-strapped program. Reimbursement rates would fall, fewer doctors and hospitals would accept Medicaid patients, and your constituents would suffer needlessly as a result.

If Congress is really determined to root out waste, fraud, and abuse you and your colleagues should spare the Medicaid program and take a hard look at the so-called “Medicare Advantage” program instead.

For more than 20 years, corporations like UnitedHealthcare have been invited to administer Medicare benefits, with disastrous results. These firms overcharge taxpayers by up to $140 billion per year, while delaying and denying care for seniors and imposing harsh restrictions that are unheard of in the traditional Medicare program.

By ending the overcharging of Medicare by corporate health insurers, Congress could recoup billions of taxpayer dollars that could be used to add dental, vision, and hearing coverage; a fully funded prescription drug benefit; and a sorely needed out-of-pocket maximum for each and every senior in the program.

Your constituents on Medicaid cannot afford cuts to their benefits. On the other hand, health insurance giants are practically swimming in profits. I urge you to take Medicaid cuts off the table and instead take aim at corporate profiteering.

Subject: Don’t cut Medicaid. Cut subsidies to corporate health insurance instead.

I am writing to you as a constituent who is concerned about the future of Medicare and Medicaid.

I am especially concerned by reports that Congress is considering significant cuts to Medicaid in order to pay for an additional round of tax cuts. This crucial public health program has been a lifeline for low-income Americans for decades, and states that have chosen to expand the program in recent years have seen gains in both population health relative to non-expansion states and financial stability for their safety net hospitals and clinics.

When the Affordable Care Act was signed into law in 2010, the federal government promised to fully fund Medicaid expansion for the first three years and to fund 90% of Medicaid expansion from 2020 onwards. This is a promise that must be kept. To do otherwise—to reduce federal funding to 70%, 50%, or even lower—would starve an already cash-strapped program. Reimbursement rates would fall, fewer doctors and hospitals would accept Medicaid patients, and your constituents would suffer needlessly as a result.

If Congress is really determined to root out waste, fraud, and abuse you and your colleagues should spare the Medicaid program and take a hard look at the so-called “Medicare Advantage” program instead.

Contact

- Rep. Julia Brownley: email, (CA-26): DC (202) 225-5811, Oxnard (805) 379-1779, T.O. (805) 379-1779

- or Rep. Salud Carbajal: email.(CA-24): DC (202) 225-3601, SB & Ventura: (805) 730-1710 SLO (805) 546-8348

- Senator Adam Schiff: email, DC (202) 224-3121, LA (310) 914-7300, SF (415) 393-0707, SD (619) 231-9712, Fresno (559) 485-7430

- and Senator Padilla: email, DC (202) 224-3553, LA (310) 231-4494, SAC (916) 448-2787, Fresno (559) 497-5109, SF (415) 981-9369, SD (619) 239-3884

- Who is my representative/senator?: https://www.usa.gov/elected-officials

What do middle and working class people need?

- Instead of doubling the rate increase for so-called “Advantage” plans, we could establish an out-of-pocket maximum for people on Medicare. (Read PNHP’s full report on how “Corporate Health Insurers Harm America’s Seniors.” It’s filled with informative videos.)

- Instead of cutting taxes for the wealthiest Americans, we could add robust dental, hearing and vision benefits for seniors.

- Instead of continuing to cede our public health programs to private-equity pirates, we can establish single-payer Medicare for All.

Deeper Dive – “Why we can’t have nice things…like the universal health care the rest of the world has.”

Health Care Insurers CEO Pay in 2023

| CEO | Company | Salary in 2023 | Profit |

| Andrew Witty | UnitedHealth Group | $20,865,106 | $20 billion |

| Joseph Zubretsky | Molina Healthcare | $22,131,256 | |

| Karen Lynch | CVS Caremark | $21,317,055 | $4.2 billion |

| David Cordani | Cigna Health Group | $20,965,504 | $6.7 billion |

| Gail Boudreaux | Elevance Health/Anthem | $20,931,081 | $6 billion |

| Bruce Broussard | Humana | $17,198,844 | |

| Sarah London | Centene Corp | $13,246,447 | |

| Maurice Smith | Health Care Service Corp. | $28,000,000 | |

| Patrick Geraghty | GuideWell | $24,600,000 | |

| Gregory Adams | Kaiser Permanente | $17,268,060 | |

| Total for (10) CEO’s | 206,523,353 | estimated $41 billion |

Interesting facts:

- Kaiser, a “non-profit” has 40 executives who make over a million dollars in salaries.

- Assuming the other “for-profits” have something similar, that’s another $400,000,000 is just executive compensation, so a rough total of [$600,000,000 in executive salaries + ±$41 billion in profits] is being drained from the system every year.

- Anthem Blue Cross Blue Shield has been consistently underpaying reimbursements and inappropriately denying coverages. In 2021, 53% of Anthem’s medical bills for the second quarter were unpaid, amounting to $2.5 billion.

- In 2023, UnitedHealth announced it was going to require prior authorization for colonoscopies. Public outcry made they reverse course.

- An American Medical Association survey found 94% of physicians surveyed said that prior authorizations lead to delays in receiving care and 80% said that prior authorizations can lead to treatment abandonment.

- The ACA put a cap on insurance profit margins, but not profit levels. Insurers are supposed to spend 80% of every dollar on care and only 20% on administrative costs. However, instead of lowering premiums, the insurance companies have been incentivized to increase costs so that they can make more money.

- Medicare – the completely government-run program (Medicare Advantage is private insurance) has only a 2% administration cost.

- Nearly 28 million Americans are still without any health insurance.

- WE ARE THE ONLY DEVELOPED COUNTRY WITHOUT UNIVERSAL HEALTH CARE!

Fish rots from the head. Our health insurance system rotted from its roots.

If the GOP, and the extreme-right Moms for Liberty have their way in erasing uncomfortable history, this question will become an insoluble mystery. That’s because the answer is rooted not just in the corporations and private-equity pirates currently taking over health care facilities and raising costs, but in one of our country’s original sins, i.e. slavery.

Federal health care policy was designed, both implicitly and explicitly, to exclude Black Americans. After straight-up racial discrimination was made illegal, the insurance industry and legislators created racially-targeted exclusionary policies based on education and occupation. These, however, would ensnare other groups as well, such as the poor rural populations and blue-collar workers. Then “pre-existing conditions” allowed them to exclude anyone they wanted to before the ACA and now they are denying care in other ways. Only the wealthiest are unaffected by the toxic insurance mechanism we’re burdened with instead of an actual system of health care. Read more complete histories here, here, and here. Article on Frederick L. Hoffman here.

- (Related to the video) “In 1896, Frederick L. Hoffman, a statistician at the Prudential Life Insurance Company, published a 330-page article in the prestigious Publications of the American Economic Association intended to prove—with statistical reliability—that the American Negro was uninsurable. Race Traits and Tendencies of the American Negro was a compilation of statistics, eugenic theory, observation, and speculation, solicited by the Prudential in response to a wave of state legislation banning discrimination against African Americans.” Despite faulty methodology and mathematical analysis, the work of this proponent of racial hierarchy and white supremacy remained influential for years, gave spurious credibility to “scientific racism,” and “embedded racial ideologies within its approach to actuarial data, a legacy that remains with the field today.”

- “Prudential’s claims that the insurance of black lives caused a drain on revenue were spurious. While the company expected financial losses, the anticipated drain was not due to differential mortality but rather to the reduction of sales to white customers assumed to be unwilling to patronize a company that considered black lives worth insuring. This calculus of social worth, financial value, public opinion, and corporate profit was one by which Prudential and other insurers had guided their strategies for a century. To sell insurance policies at equal rates or for equal benefits across racial lines would offend a predominant system of social beliefs about the worth of human lives. But at the same time, only a scientific, statistical explanation could be used in the age of progress to publicly explain Prudential’s decision.“

- Social Security and Wagner Acts of 1935 (the Wagner Act ensured the right of workers to collective bargaining), and the Fair Labor Standards Act of 1938, which set a minimum wage and established the eight-hour workday deliberately excluded farm and domestic workers — more than half the nation’s Black work force at the time.

- Aid to Dependent Children and the 1944 Servicemen’s Readjustment Act, better known as the G.I. Bill, allowed state leaders to exclude Black people.

- The Hill-Burton Act provided federal grants for hospital construction to communities in need, but ensured that states controlled the disbursement of funds and could segregate resulting facilities.

- American Medical Association barred Black doctors; medical schools excluded Black students, and most hospitals and health clinics segregated Black patients. Medicare and Medicaid finally brought the legal segregation of hospitals to an end.

- By the 1950s, [Black organizations] were pushing for a federal health care system for all citizens. That fight put National Medical Association (the leading Black medical society) into direct conflict with the A.M.A., which was opposed to any nationalized health plan.”

- Employer-based insurance went with jobs that wouldn’t hire Black people.

- 1964 Civil Rights Act outlawed segregation, new health care programs excluded millions of Americans by specific age, employment or income groups, in ways that were highly correlated to race. However, they also applied to many poor and blue-collar White workers.

- Historically biased insurance rules include redlining, restrictive covenants, race-based insurance premiums, and what advocates call subtle proxies for unfair discrimination, such as using ZIP codes and credit scores to price auto insurance.

- The biggest beneficiaries of the Affordable Care Act were people of color who obtained coverage through Medicaid expansion. Several states, most of them in the former Confederacy, refused to participate in Medicaid expansion. And several are still trying to make access to the program contingent on onerous new work requirements.

Why single-payer?

GoFundMe is a warning.

When the crowdfunding platform started, it was aiming for “ideas and dreams,” “wedding donations and honeymoon registry” or “special occasions.” Said CEO Rob Solomon, “We didn’t build the platform to focus on medical expenses,…The reality is, though, that access to health care is connected to the ability to pay for it. If you can’t do that, people die. People suffer.

I guess what I realized [when I came] to this job is that I had no notion of how severe the problem is. You read about the debate about single-payer health care and all the issues, the partisan politics. What I really learned is the health care system in the United States is really broken. Way too many people fall through the cracks.

The system is terrible. It needs to be rethought and retooled. Politicians are failing us. Health care companies are failing us.”

America is not #1 in the world for healthcare. In fact, according to the Legatum Institute, a London-based think tank, we are listed at #69, ahead of Algeria and Mexico and humiliatingly behind Armenia. We rank high on technology, but if you can’t access health care, that is of little importance. The Comonwealth Institute put us at #11, last among 11 high-income countries (Australia, Canada, France, Germany, the Netherlands, New Zealand, Norway, Sweden, Switzerland, the United Kingdom, and the United States). Despite spending far more per patient, we fail on how easily people can access care, administrative procedures and equity around this care, and the quality of healthcare outcomes

- We have 30 million uninsured, including 1 of every 10 kids.

- Americans likely owe hundreds of billions of dollars in total medical debt, with millions, owing more than $10,000. Black adults, those in poor health, and people living with disabilities are most likely to carry significant medical debt

- Millions can’t find doctors.

- Average wait time is 26 days.

- UPDATE: Emergency wards are understaffed and people are dying in the waiting rooms.

(Snopes) “The United States may regard itself as a “leader of the free world,” but an index of development released in July 2022 places the country much farther down the list.

In its global rankings, the United Nations Office of Sustainable Development dropped the U.S. to 41st worldwide, down from its previous ranking of 32nd. Under this methodology – an expansive model of 17 categories, or “goals,” many of them focused on the environment and equity – the U.S. ranks between Cuba and Bulgaria. Both are widely regarded as developing countries.

The Affordable Care Act still isn’t affordable enough…

From KFF: Americans’ Challenges with Health Care Costs

- About half of U.S. adults say they have difficulty affording health care costs. About four in ten U.S. adults say they have delayed or gone without medical care in the last year due to cost, with dental services being the most common type of care adults report putting off due to cost.

- Substantial shares of adults 65 or older report difficulty paying for various aspects of health care, especially services not generally covered by Medicare, such as hearing services, dental and prescription drug costs.

- The cost of health care often prevents people from getting needed care or filling prescriptions. About a quarter of adults say they or family member in their household have not filled a prescription, cut pills in half, or skipped doses of medicine in the last year because of the cost, with larger shares of those in households with lower incomes, Black and Hispanic adults, and women reporting this.

- High health care costs disproportionately affect uninsured adults, Black and Hispanic adults, and those with lower incomes. Larger shares of U.S. adults in each of these groups report difficulty affording various types of care and delaying or forgoing medical care due to the cost.

- Those who are covered by health insurance are not immune to the burden of health care costs. About one-third of insured adults worry about affording their monthly health insurance premium, and 44% worry about affording their deductible before health insurance kicks in.

- Health care debt is a burden for a large share of Americans. About four in ten adults (41%) report having debt due to medical or dental bills including debts owed to credit cards, collections agencies, family and friends, banks, and other lenders to pay for their health care costs, with disproportionate shares of Black and Hispanic adults, women, parents, those with low incomes, and uninsured adults saying they have health care debt.

- Affording gasoline and transportation costs is now a top worry for Americans followed by unexpected medical bills. While worry over gasoline and transportation costs has risen markedly since 2020, significant shares of adults still say they are worried about affording medical costs such as unexpected bills, deductibles, and long-term care services for themselves or a family member.

How insurers still manage to screw us over in the age of the Affordable Care Act.

(ProPublica)”Company doctors then sign off on the denials in batches, according to interviews with former employees who spoke on condition of anonymity.

“We literally click and submit,” one former Cigna doctor said. “It takes all of 10 seconds to do 50 at a time.”

“Cigna emphasized that its system does not prevent a patient from receiving care — it only decides when the insurer won’t pay. “Reviews occur after the service has been provided to the patient and does not result in any denials of care,” the statement said.”

Just medical bankruptcies… the number-one cause of U.S. bankruptcies.

In the dark days before the Affordable Care Act, health care insurers kicked sick people off plans with recission and benefit caps, and denied care for “pre-existing conditions. Now, under the ACA, they are using algorithms to deny claims in bulk, in ever-increasing numbers, with very few people fighting back.

They are hoping that a GOP-controlled congress, where 183 Republicans voted against H.R. 986 – Protecting Americans with Pre-existing Conditions Act of 2019, the will bring back their previous weapons against us. (Watch what they do, not what they say!) Pre-existing conditions affect as many a 1 in 2 Americans. Because of the Affordable Care Act, they cannot be denied coverage, be charged significantly higher premiums, be subjected to an extended waiting period, or have their benefits curtailed or capped by insurance companies. But that could change with one election.

BTW, If you had COVID, that would count as a “pre-existing condition.”

UPDATE 08/09/23: Read “Request Denied“: “If you are having claims denied – we have resources below for appealing the denials. Some states will even help you by arranging a third party review for you. If your appeal to the insurance company is rejected you may want to contact the insurance commissioner in your state. This website can get you their phone number.”

How insurers still manage to screw us over in the age of the Affordable Care Act.

(ProPublica)”Company doctors then sign off on the denials in batches, according to interviews with former employees who spoke on condition of anonymity.

“We literally click and submit,” one former Cigna doctor said. “It takes all of 10 seconds to do 50 at a time.”

“Cigna emphasized that its system does not prevent a patient from receiving care — it only decides when the insurer won’t pay. “Reviews occur after the service has been provided to the patient and does not result in any denials of care,” the statement said.”

Just medical bankruptcies… the number-one cause of U.S. bankruptcies.

In the dark days before the Affordable Care Act, health care insurers kicked sick people off plans with recission and benefit caps, and denied care for “pre-existing conditions. Now, under the ACA, they are using algorithms to deny claims in bulk, in ever-increasing numbers, with very few people fighting back.

They are hoping that a GOP-controlled congress, where 183 Republicans voted against H.R. 986 – Protecting Americans with Pre-existing Conditions Act of 2019, the will bring back their previous weapons against us. (Watch what they do, not what they say!) Pre-existing conditions affect as many a 1 in 2 Americans. Because of the Affordable Care Act, they cannot be denied coverage, be charged significantly higher premiums, be subjected to an extended waiting period, or have their benefits curtailed or capped by insurance companies. But that could change with one election.

BTW, If you had COVID, that would count as a “pre-existing condition.”

UPDATE 08/09/23: Read “Request Denied“: “If you are having claims denied – we have resources below for appealing the denials. Some states will even help you by arranging a third party review for you. If your appeal to the insurance company is rejected you may want to contact the insurance commissioner in your state. This website can get you their phone number.”

“Prior Authorization”: a system that delays or refuses treatment, disparages doctors and wastes man-hours

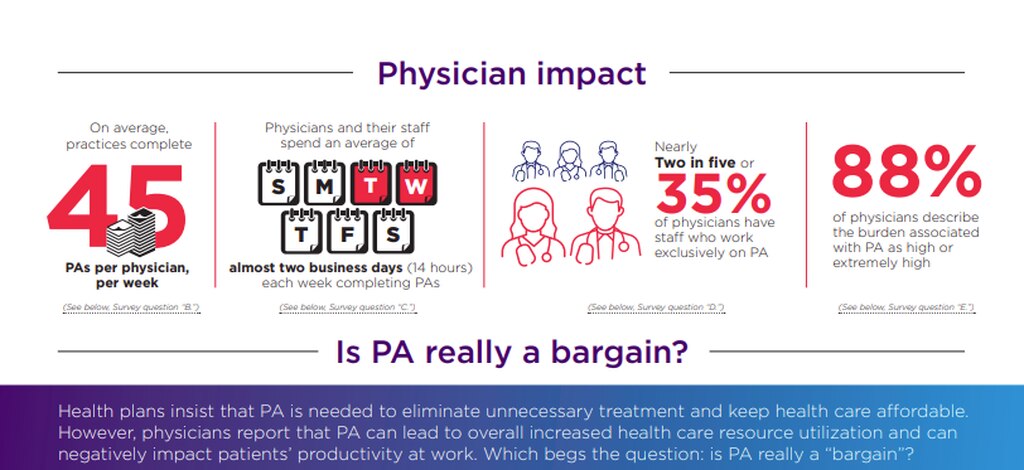

(Investigatetv.com) “In a 2022 American Medical Association survey of physicians, responding doctors reported an average of 45 requests per-physician, per-week, up from an average of 31 per-week reported in the 2018 survey. The previous year’s survey found 84% of respondents said they’d seen an increase in the number of prior authorizations required over the preceding five years.” This is time that doctors can’t spend with you, the patient.

“According to the AMA survey, physicians and their staffs spend an average of 14 hours, or nearly two business days, processing prior authorization requests and any associated appeals. Nearly two in five physicians said they have a staff member solely dedicated to prior authorization.

“That’s time that we, frankly, just don’t have,” said Dr. Gabe Charbonneau, a Montana family physician and co-founder of the grassroots organization Medicine Forward, which along with

What do American businesses need?

Oh, yeah, Medicare-for-All. How can American companies compete on an equal level against companies in countries that don’t have to spend so much time and money figuring out health care insurance for their employees?

How can our companies compete against foreign companies who don’t have large outlays for employee health benefits. How can small employers compete against larger employers for the best workers?

The exception to the pain, of course, those involved in the private healthcare insurance industry.

“CVS Health CEO Karen Lynch takes the top spot in our annual look at compensation for CEOs at the six major national insurers, bringing in $21.3 million in total compensation last year, according to annual proxy filings with the Securities and Exchange Commission.

The six CEOs together earned more than $114.5 million in total compensation, according to the filings.“

Each of America’s 30 million uninsured could have amazing medical care every year with enough left over to prevent some medical bankruptcies. How many scholarships for doctors and nurses could have been provided? How many dental checkups, hearing aids or health screening does that represent?

More details on CA state health care issues

(Nation) “Reports from the Healthy California for All Commission, a single-payer health care task force appointed by the state government, estimate that the present system, characterized by huge inequities, coverage gaps, restrictions on access to care, and administrative complexity, will cost an estimated $323–$496 billion more in 2031 than would a single-payer system covering everybody. That means every Californian adult and child would pay $8,000–$12,000 more for health care than we should.

We see the same dynamic in debates over Medicare for All at the national level. In 2020, economists at the University of California–San Francisco reviewed 22 national health care financing studies, and found that 20 of them demonstrated savings through a single-payer model. The nonpartisan Congressional Budget Office, meanwhile, determined that federally Medicare for All would generate $650 billion in savings.

But what about taxes, the favorite scare tactic of those who profit from the current dysfunctional system? According to a study from the Healthy California for All Commission, it turns out that the current cost of health care is the biggest “tax” paid by the middle class—ranging from 25 to 40 percent of a household’s income. Single-payer financing eliminates that burden. Replacing the cost of premiums, co-payments and deductibles with modest public tax increases on businesses and high-income individuals seems like a very good deal.”

Resources

- (USW.org) 183 Republicans vote against bill to protect people with pre-existing conditions

- (healthysystemtracker.org) How does the quality of the U.S. health system compare to other countries?

- (stanmed.stanford.edu) Insurance Policy – How an industry shifted from protecting patients to seeking profit.

- (healthsystemtracker.org) How does health spending in the U.S. compare to other countries?

- (pgpf.org) HOW DOES THE US HEALTHCARE SYSTEM COMPARE TO OTHER COUNTRIES?

- (cnn.com) US spends most on health care but has worst health outcomes among high-income countries, new report finds

- (Statnews) Long waits to see a doctor are a public health crisis

- (fiercehealthcare.com) Universal healthcare in U.S> would have saved 212,000 lives, $459B in 2020, study finds.

- (KFF) Americans’ Challenges with Health Care Costs

- (KFF) Key Facts about the Uninsured Population

- (KFF) Sen. Sanders Says Millions of People Can’t Find a Doctor. He’s Mostly Right.

- (KFF) The Burden of Medical Debt in the United States

- (KFF) 1 in 10 Adults Owe Medical Debt, With Millions Owing More Than $10,000

- (Statnews) Private equity, health care, and profits: It’s time to protect patients

- (PNHP) Physicians for a National Health Care Plan

- (PNHP) Financing a single-payer national health program

- (PNHP) The Medicare for All Act of 2023

- (nasi.org) History of Medicare

- (CalMatters) Why single-payer advocates are split on how to overhaul health care

- (CalMatters) Slow roll to finish California budget

- (leginfo.legislature.ca.gov) SB-770 Health care: unified health care financing.

- (sd11.senate.ca.gov) SENATOR WIENER ANNOUNCES NEW LEGISLATION TO SEEK FEDERAL WAIVERS FOR A SYSTEM OF GUARANTEED HEALTHCARE

- (LATimes) After ambitious single-payer healthcare plans sputter, a new California bill tries an incremental approach

- (leginfo.legislature.ca.gov) AB-1690 Universal health care coverage.

- (nationalnursesunited.org) A.B. 1690 CALIFORNIA GUARANTEED HEALTH CARE FOR ALL ACT – Ash Kalra

- (abc7) CalCare: Single-payer health care in California still years away – There are many questions about a system that would move everyone in California off their current plans and onto a single plan.

- (congress.gov) S.1655 – Medicare for All Act

- (aafp.org) After ambitious single-payer healthcare plans sputter, a new California bill tries an incremental approach

- (KFF) GoFundMe CEO: ‘Gigantic Gaps’ In Health System Showing Up In Crowdfunding

- (Nation) The Plan to Save Californians $117 Billion a Year by Switching to Single-Payer – Why is universal health care seen as prohibitively expensive when the status quo costs far more?

- (PBS)

- (ProPublica) How Cigna Saves Millions by Having Its Doctors Reject Claims Without Reading Them

- (www.cms.gov/) At Risk: Pre-Existing Conditions Could Affect 1 in 2 Americans: 129 Million People Could Be Denied Affordable Coverage Without Health Reform

- (KFF) Is COVID-19 a Pre-Existing Condition? What Could Happen if the ACA is Overturned

- (Internationalinsurance) What are the Countries with the Best Healthcare?

- (snopes) US Is Becoming a ‘Developing Country’ on Global Rankings That Measure Democracy, Inequality

- (Washington Post) Private equity investors raising U.S. medical prices, study says – Researchers examined the effects of private equity firms buying up physician practices

- (Forbes) Private Equity And The Monopolization Of Medical Care

- (Alan Unell Ph.d) Emergency in The Emergency Department

Resources for Racism in Health care

- (PNHP) Race as a barrier to universal health care – Why doesn’t the United States have universal health care? The answer has everything to do with race.

- (courageousconversation) Why Doesn’t the United States Have Universal Health Care? The Answer Has Everything to Do With Race.

- (LAProgressive) One Reason Why America Doesn’t Have Universal Healthcare

- (NLG.org) The Color of Pain: Blacks and the U.S. Health Care System – Can the Affordable Care Act Help to Heal a History of Injustice? Part I

- (ncbi.nlm.nih.gov) The Myth Of The Actuary: Life Insurance And Frederick L. Hoffman’s Race Traits And Tendencies Of The American Negro

- (floir.com) Report of Commissioner, Kevin M. McCarty

- (investopedia.com) Discrimination in Insurance Underwriting Guidelines